In a financial landscape evolving with the rapid ascent of Bitcoin, traditional banks grapple with the transformative potential of digital assets. While skepticism persists, regulatory bodies are navigating the delicate balance between risks and rewards in the Bitcoin ecosystem.

Several central banks and federal savings associations are now empowered to leverage public blockchains and stablecoins for payment activities, positioning Bitcoin as a catalyst for quicker, more efficient payments.

Contents

Potential Impact of Bitcoin on Traditional Banking

Bitcoin has emerged as a transformative force with the potential to reshape the landscape of traditional banking. Their impact extends across various dimensions, offering both challenges and opportunities for financial institutions.

Alternative Banking Systems

Bitcoin presents a formidable alternative to conventional banking systems, challenging the established order. This shift could result in a diminished reliance on traditional banks, fostering a dynamic where peer-to-peer transactions occur seamlessly through payment apps.

Consequently, the envisaged outcome includes reduced fees and heightened efficiency in financial transactions.

Consumer Behavior and Transactional Dynamics

Bitcoin wields the power to influence consumer behavior and redefine transactional processes. Its inherent attributes—speed, cost-effectiveness, and security—could drive increased adoption by consumers.

The decentralized nature of the digital currency may also trigger changes in transactional methodologies, liberating processes from the constraints of traditional financial institutions.

Revolutionizing Cross-Border Transactions

The innovation in payment systems, spearheaded by Bitcoin, promises a revolution in transaction paradigms. The potential for faster, more cost-effective domestic and cross-border transactions holds the key to enhancing global financial accessibility.

Notably, individuals in remote or underserved areas, devoid of traditional banking services, can now seamlessly engage in financial activities such as transferring money or making payments through digital banking platforms. This transformation underscores the role of digital currencies, particularly in reshaping international remittances.

Disruption in Business Models

The ascent of Bitcoin has the potential to disrupt traditional banking business models significantly. Operating on decentralized systems, digital currencies eliminate the need for financial institutions as intermediaries, fostering transactions through diverse digital payment applications.

This disruption, termed disintermediation, foresees a scenario where traditional banks witness a decline in revenue, particularly from services like currency exchange and international money transfers.

Why Do Banks Lose Sleep Over Bitcoin?

The rise of Bitcoin presents a dual challenge and opportunity spectrum for traditional banks. On one hand, the prospect of disintermediation and a potential reduction in revenue looms large.

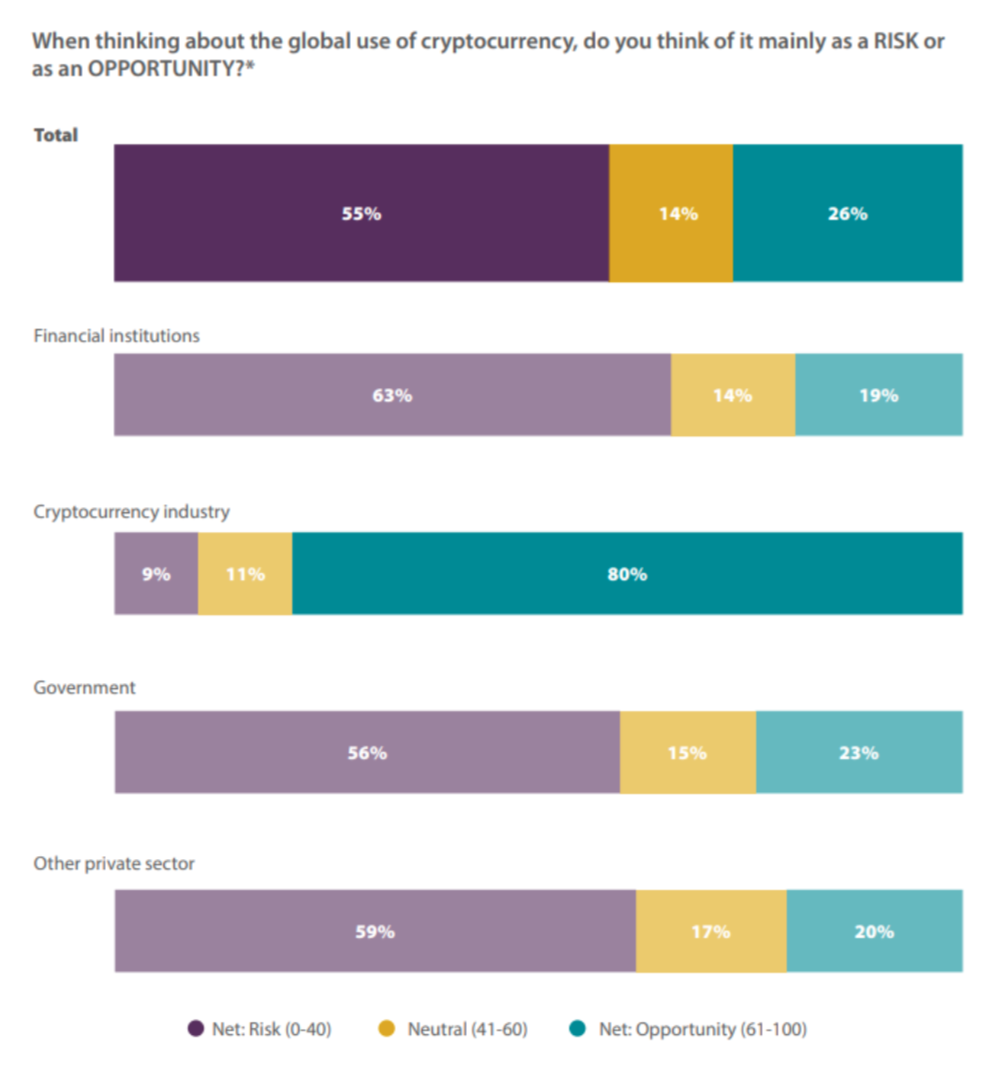

Despite the potential benefits, banks remain cautious about embracing Bitcoin. A survey by the Association of Certified Anti-Money Laundering Specialists (ACAMS) and the U.K.’s Royal United Services Institute reveals that 63% of banking professionals view digital assets as a risk rather than an opportunity.

Here are some of the challenges that banks face when it comes to adopting bitcoin:

- Bitcoin’s decentralized nature challenges the established central banking structure, which gives control to a few hands. This raises concerns about the future role of traditional banks.

- Bitcoin transactions’ pseudonymous nature poses challenges for Anti-Money Laundering (AML) and Know-Your-Customer (KYC) compliance, fueling apprehensions about potential illicit activities.

- Historical volatility in bitcoin’s prices adds to banks’ apprehension, casting doubt on the viability of digital currencies as stable investment vehicles.

Embracing Bitcoin: A Vision for the Future of Finance

As the use of Bitcoin continues its upward trajectory, governments are expected to refine regulations and oversight, aiming to curb fraud and ensure consumer protection in Bitcoin transactions. This evolving landscape presents both challenges and opportunities for traditional banks.

Recent industry moves, such as the introduction of spot bitcoin Exchange-Traded Funds (ETFs) by major traditional financial firms, underscore a growing acceptance of digital currencies.

Integration Strategies for Banks

Traditional banks can actively engage with the Bitcoin revolution through strategic integration:

- Custody Services: Banks can offer secure custody services for Bitcoin, holding either the digital asset itself or the cryptographic keys for private wallets.

- Onboarding and Assistance: Banks can develop user-friendly tools to simplify the onboarding process for new Bitcoin investors. They can provide expert assistance for those unfamiliar with setting up wallets. Introduce interest-bearing Bitcoin accounts, enabling customers to invest through various financial tools.

- AML/KYC Regulations: Adherence to AML and KYC regulations for Bitcoin transactions is essential. Exploring the potential of automating these verifications using blockchain technology for a streamlined customer data view is crucial.

- Streamlined Payments: Banks can use the Bitcoin network to expedite payment processes and embrace faster and more cost-effective clearing and settlements, enhancing transaction speed.

- Smart Contracts Implementation: Reinforce trust by acting as a reliable third party for smart contracts in Bitcoin transactions. Explore the use of smart contracts for mortgages, commercial loans, letters of credit, and other financial agreements.

The future of finance is intertwined with the adoption and integration of Bitcoin. Traditional banks, rather than perceiving Bitcoin as a threat, can unlock new possibilities by embracing it as a transformative force.